Dynamic Factor Rotation for Quantitative Investment

Dynamic factor rotation strategy for SSE 50 constituents using market regimes and time-series prediction.

Dynamic Factor Rotation for Quantitative Investment

This course project studied factor rotation in quantitative investment. It constructed factor long-short returns for Shanghai Stock Exchange 50 constituents and used market-regime analysis plus prediction models to dynamically allocate factor weights.

What It Does

- Builds monthly long-short factor return series for momentum, value, quality, volatility, and size factors.

- Identifies market regimes using index returns, volatility, and trading-volume features.

- Uses time-series modeling to predict next-period factor performance.

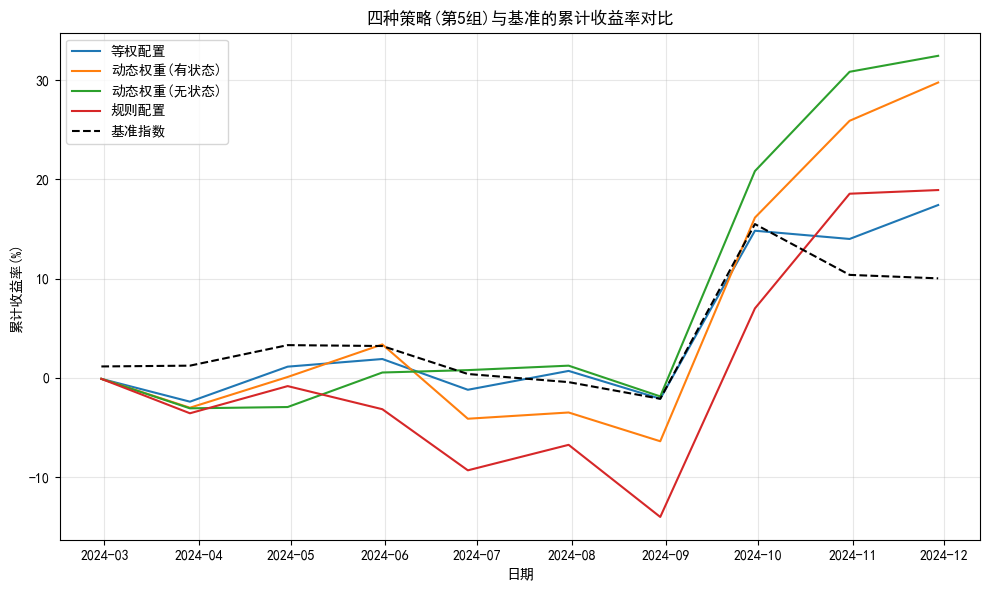

- Converts predicted factor returns into dynamic weights and compares the strategy against static and rule-based baselines through backtesting.

Research Logic

The project follows a pipeline: market states exist, factor performance depends on those states, factor rotation is therefore meaningful, and dynamic weighting may improve risk-adjusted performance.

Tech Stack

Python, Jupyter Notebook, NumPy, pandas, scikit-learn, LSTM experiments, factor backtesting workflow.